The economic, social and environmental benefits of the industrial & logistics sector

The pandemic, lockdowns, and supply chain issues of the past two years have made it abundantly clear that warehousing and industrial logistics facilities are critical to the UK’s infrastructure.

Alongside the road, rail, air-freight and port facilities, industrial warehousing and logistics are essential to moving goods around the country.

The sector has also been a source of essential jobs and economic activity, as other sectors have shut down – particularly in regions in the North of England and the Midlands.

A new report from the BPF (British Property Federation), Savills, and the UKWA (United Kingdom Warehousing Association) advocates for a planning system that is more responsive to the needs of the industrial and logistics sector.

The industrial & logistics sector as an economic powerhouse

The UK’s industrial and logistics sector provides economic, social and environmental benefits to the nation.

Industrial and logistics facilities are essential to our economic growth, supporting the supply of critical goods like fuel, food and medical supplies.

As an ‘economic powerhouse’, the industrial and logistics sector generates economic benefits, including £232 billion of GVA (gross value added) – a 14% share of total economy – and 2.8 million industrial and logistics jobs in England.

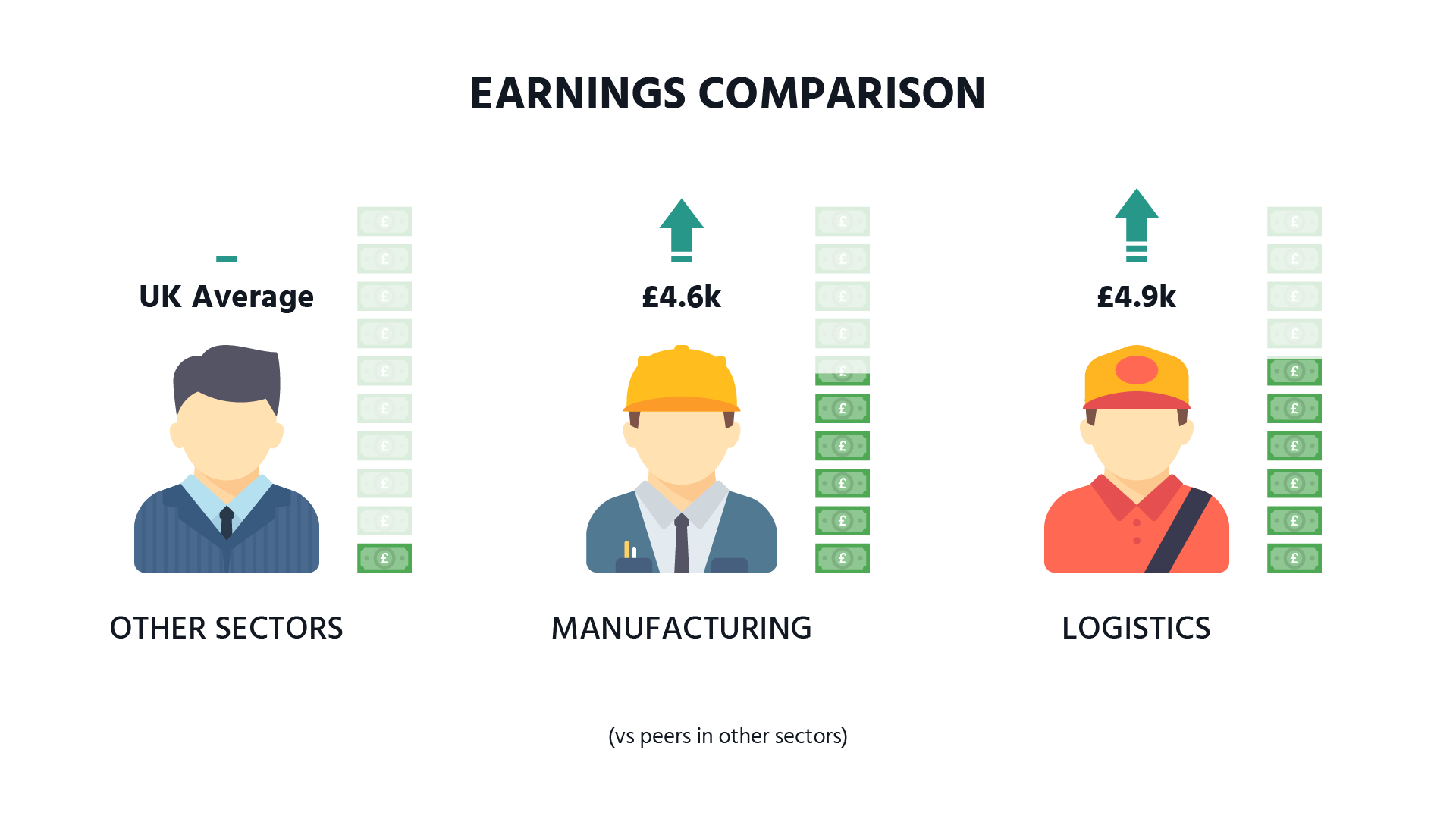

There are still some widespread misconceptions about the types of jobs, pay and skills in the sector.

However, the reality is that jobs in the sector demand highly skilled workers, and pay more on average than equivalent roles in other sectors. Workers in manufacturing earn around £4.6K more per year than their peers in other sectors, and workers in logistics earn around £4.9K more per year than their peers in other sectors.

“A key finding of our report is a historic lack of warehouse supply has restricted demand by 29% nationally. We estimate that future demand for logistics space will be at least 40% higher in Leeds, 35% higher in Manchester and 29% higher in Birmingham.”

– Mark Powney, Director of Economics, BPF

The industrial & logistics sector as an employment driver

As well as on-site jobs the industrial and logistics supply chain provides significant levels of employment across the UK:

- UK freight arrives via ports and airports

- Freight is handled at port or air-side sheds before distribution

- Besides the transport crew or drivers, there are also workers who build or maintain the vans, aircraft, trains etc.

- Goods are moved mainly by HGV, LGV or rail, either to distribution hubs or DTC (direct to customers)

- The end customers may be homes or other businesses

Levelling up the industrial & logistics sector

The government’s Levelling Up plan aims to spread opportunity and prosperity to all parts of the UK.

Investment in the industrial and logistics sector is helping to support that agenda, with 70% of demand (and jobs) generated in the North and Midlands, compared to just 30% in the South.

Industrial and logistics investment can even aid in the delivery of new housing, via the funding of strategic infrastructures such as motorway junction upgrades and link roads which can serve both residential and industrial and logistics.

“Our research also finds that the sector supports 3.8 million jobs, a 29% rise in productivity is expected by 2039, and wage rates are rising quicker than in many other sectors”

– Kevin Mofield, Head of EMEA Industrial & Logistics Research, Savills

The environmental benefits of the UK’s industrial and logistics sector

There are three sources of carbon across the lifecycle of industrial and logistics properties:

Embodied carbon

This can include the processing and transportation of raw materials, as well as the carbon emitted by construction.

Modern industrial and logistics facilities are being built with recycled, low carbon and sustainably sourced materials. They are achieving results like Net Zero Carbon recognition, and top EPC and BREEAM ratings.

Operational carbon

The carbon produced during the day-to-day operations of a property. Modern industrial and logistics facilities are innovating in myriad ways to reduce carbon:

- Alternative energy generation, with wind turbines, solar energy, geothermal energy, and harvested rainwater

- Energy-saving measures like green roofs, LED motion-sensing lights, smart metres, and facade insulation

- Sustainable materials like cement alternatives and sustainable facades

- Innovative use of roof space, with skylights, green roofs and solar PVPs

- Charging points for HGVs and LGVs

- Smart use of indoor space, with co-location of offices and outdoor gym trails

- Staff parking for alternative modes of transport (like bikes or EVs)

- Outdoor spaces with hedgerows, stone walls, locally sourced planting, ponds, bird nesting boxes, wildflower meadows, and beehives, to encourage wildlife.

End of life carbon

Modern industrial and logistics buildings continue to have a life long after their use as a logistics facility. Lightweight structures are highly adaptable for use as warehouses, temporary hospitals, leisure & gym facilities, data centres, and lab spaces.

Once their lifecycle is truly at an end, the steel frames used in industrial and logistics properties are much more easily recycled than the concrete used for other commercial buildings.

“As our economy rebounds from COVID-19, the industrial and logistics sector will help to ensure a green recovery as buildings continue to achieve net-zero status and contribute to the greening of supply chains”

– Ben Taylor, Planning Director, Newlands & Vice Chair, BPF Industrial Committee

Want to read more blog articles about logistics?

As you would expect of a transport and logistics software provider, we’ve written lots and lots of articles over the years about, well, logistics. Here’s a selection of articles you might want to read on our favourite subject:

A look at the term ‘empty miles in logistics‘; what the impact is on your business and, most importantly, what logistics businesses can do to avoid them.

‘What is Track and Trace in Logistics‘ aims to define what that means in the food manufacturing and pharmaceutical industry (and is something that Stream does exceptionally well).

And finally, if you’re interested in route planning fixed routes, then this article, ‘What is a ‘Milk Run’ in logistics?’ is the one for you.

You could also have a read of this article which looks at the reasons why modern logistics is in fact cloud-based (like Stream for instance.