The transition towards sustainable fleets en masse is at a crucial point, with businesses facing both big challenges and opportunities as they progress towards alternative, sustainable fuels to power their vehicles.

Teletrac Navman’s latest sustainability survey, Mobilising The Future of Fleets: 2025 Energy Edition, conducted in November 2024, gathered insights from 536 respondents across Australia, New Zealand, Mexico, the United Kingdom, and the United States.

It reveals a diverse range of opinions from the industry, ranging from eagerness and readiness for decarbonisation to serious concerns about its practicality, cost, and government legislature(s) or initiatives.

Despite ongoing operational and financial pressures, many fleet operators are actively researching and looking to implement sustainable solutions, largely driven by customer demand and the desire to improve their brand reputation.

The report covers fuel costs and operational strategies, factors driving decarbonisation and fleet transition, current progress of fleet transition and changing fleet composition, respondent sentiment analysis, and the evolving landscape of fleet sustainability.

Foreword by Alain Samaha, CEO of Teletrac Navman

Alain Samaha, CEO of Teletrac Navman, offers a foreword to the report, emphasising that sustainability and decarbonisation are among the most pressing issues facing the fleet industry today, with no single agreed-upon solution:

“While some fleet operators see decarbonisation as an opportunity to reduce costs and strengthen customer trust, others remain sceptical, viewing transition as a financial strain or an unrealistic regulatory expectation.”

Many businesses also question whether net-zero targets are feasible, stressing the need for clearer data, stronger financial incentives, and practical strategies for real-world operations.

The wider industry is grappling with how to make informed sustainability decisions, identify effective solutions, and balance environmental goals with commercial realities and economic viability.

And so the industry is posing key questions:

• With so many challenges and competing priorities, how can I make informed decisions about sustainability?

• What solutions will deliver real impact?

• How can I balance environmental goals with commercial realities?

The report aims to explore these critical questions, offering insights into the industry’s current perspectives and the key obstacles the participants in the study believe are hindering progress.

Samaha hopes that “by understanding these perspectives, fleet operators, industry leaders and policymakers can work together to drive practical, achievable change.”

Fuel costs and operational strategies

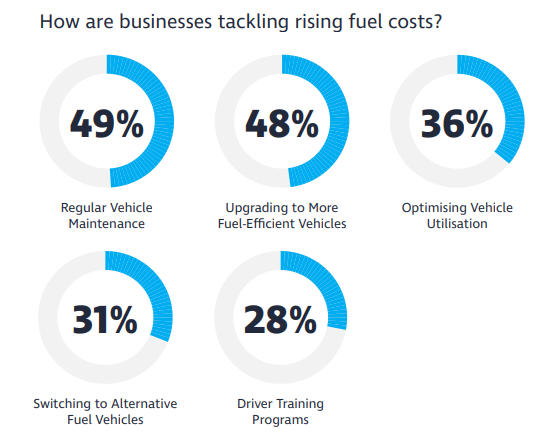

The industry is using a multi-pronged approach to combat rising fuel costs, with 74% of fleet operators surveyed in the study putting a number of strategies into practice.

Regular maintenance remains the most common countermeasure (49%) to combat rising fuel costs, which the participants widely recognised as an effective way of improving fuel efficiency, in addition to adopting more fuel-efficient vehicles (48%).

Despite these efforts, only 40% of operators are successfully meeting their fuel cost reduction goals, indicating a need for strategies beyond traditional methods as maintaining previous savings levels becomes increasingly difficult.

Additionally, 61% of businesses are making CapEx investments to address rising fuel costs.

When asked about current approaches to managing fuel costs, 49% use regular vehicle maintenance, 48% upgrade to more fuel-efficient vehicles, 36% optimise vehicle utilisation, 31% switch to alternative fuel vehicles, and 28% implement driver training programmes, reflecting a diverse range of strategies.

Overall, 12% find their approaches extremely effective, 28% find them very effective, 58% find them somewhat effective, while 2% find them not effective at all, suggesting mixed sentiment.

Decarbonisation and fleet transition

Rising fuel costs have the potential to divert investment, resources, and overall openness from transitioning to sustainable, alternative practices, as businesses juggle immediate operational needs with long-term sustainability objectives.

Beyond cost worries, other significant drivers for fuelling the transition to sustainable practices include environmental pressures, with 62% of operators acknowledging the need for action and 58% citing brand and sustainability goals as factors influencing their investment in decarbonisation.

This figure increases to 79% among businesses already transitioning.

Furthermore, 63% of operators reported that customer demand has influenced their decarbonisation strategies and appetite for adoption, emphasising the growing importance of sustainability in customer relationships – when asked if customer demand has influenced the speed of decarbonisation plans, 63% said yes, 19% said no, and 18% were unsure.

Regarding environmental pressure to transition to alternative fuels, 25% strongly agree, 37% agree, 26% are unsure, 7% disagree, and 5% strongly disagree.

Other factors influencing fleet energy transition include incentives and subsidies (34%), energy security and independence (30%), government mandates (29%), corporate social responsibility (27%), and increased infrastructure availability (25%).

Progress in fleet transition

Fleet operators are at various stages of their energy transition.

According to the study, 17% are in the analysis phase, 22% are in the early execution phase, and 50% are in advanced stages. Among those in transition, 46% are assessing vehicle suitability, with 8% seeking external consultancy.

However, only 30% have completed a Total Cost of Ownership (TCO) analysis, a crucial step that is advised in order to avoid costly errors and aid overall decision-making.

Larger organisations are leading the transition to sustainable solutions, with 62% of fleets having over 50 vehicles already transitioning to eco-friendly alternatives.

Smaller organisations, particularly 39% of fleets with less than 10 vehicles, may soon feel pressure to avoid falling behind or missing out on demand for sustainable services.

The primary challenge for 56% of respondents is the high purchase costs of eco-friendly vehicles, followed by the installation costs of EV chargers and the perceived high cost of ownership.

This combined capital expense of managing rising fuel costs while transitioning to greener energy presents a significant financial hurdle, especially for smaller businesses with tighter budgets and cash flow issues.

Key actions influencing fleet energy transition include vehicle suitability assessment (46%), gradual end-of-life replacement (42%), exploring other fuel types (33%), investing in charging infrastructure (30%), and lifecycle cost analysis (30%).

Changing fleet composition

Despite increasing momentum and willingness to adopt sustainable fuel alternatives, 66% of fleets still rely on petrol or diesel vehicles. Among the 34% adopting alternative fuels, electric vehicles are leading the transition, while 30% are also incorporating gaseous or other renewable energy sources.

This indicates a diverse approach to sustainability and highlights the need for flexible infrastructure, policy support, and strategic planning to manage the evolving energy mix.

The shift to multi-energy fleets is accelerating, with 61% of operators currently using more than one vehicle energy type. In fact, 32% of fleets now operate three or more energy sources, reflecting the increasing complexity of fleet management as businesses navigate decarbonisation.

Momentum is somewhat building, too, with 8% of fleets having already transitioned at least 50% of their vehicles to alternative fuels.

Looking ahead, 48% of operators expect to reach this milestone within the next two years, signalling a significant shift in fleet energy strategies.

Additionally, 85% of fleets anticipate that at least half of their vehicles will be powered by alternative energy sources within five years, underscoring the industry’s strong commitment to sustainability and the growing feasibility of alternative fuel solutions.

Of the alternative fuels fleets have already adopted, 39% use biodiesel or renewable diesel, 37% natural gas, 23% BEV, and 15% PHEV.

Respondent sentiment analysis

Sentiment surrounding the transition to alternative fuels and decarbonisation is polarised, with a range of opinions expressed across several key areas. The survey included open-ended comments for sentiment analysis, revealing four main themes:

- Polarisation around climate change and decarbonisation

Some respondents dismiss the urgency of decarbonisation and challenge the legitimacy of climate change. Others view the transition positively, stating that “we have to all eventually do this” and that “transitioning our fleet to clean energy has increased customer trust”.

- Feasibility concerns

Many cite the financial strain of transitioning to EVs and alternative fuels due to high upfront costs, limited government incentives, and expensive ongoing operations. Operators in remote areas (particularly in Australia, New Zealand, and the U.S.) struggle with a “lack of viable charging/fuelling stations” and “inadequate infrastructure for HGVs and long-haul routes”. This contributes to persistent concerns about limited range and payload capacity compared to diesel lorries, especially for long-distance and heavy-duty operations.

- Scepticism around timelines

Many believe that government net-zero deadlines are unrealistic given the costs and logistical challenges of fleet-wide transitions. In the U.S., some operators are delaying fleet changes, waiting for political shifts, with comments such as “waiting for the next administration” to be confirmed.

- Inefficient support structures

Fleet operators desire clearer data on the total cost of ownership and real-world operational challenges of alternative fuels. Many believe current subsidies and incentives do not adequately support heavy-duty fleets or address their specific operational needs. Respondents indicated that better funding and incentives would make them more inclined to transition.

The evolving landscape of fleet sustainability

The sustainability landscape for fleets is rapidly changing, with businesses navigating financial, operational, and regulatory challenges. Despite concerns about cost and infrastructure, many operators perceive decarbonisation as a strategic advantage driven by customer expectations and brand positioning.

While the transition to alternative fuels is gaining momentum, the pace and feasibility of adoption remains a key debate. Some operators are optimistic about the shift, anticipating significant progress in the next five years, while others remain cautious due to financial pressures, infrastructure accessibility, and regulatory uncertainties.

As fleets navigate these complexities, access to accurate data and actionable insights will be crucial for making informed decisions that align with both business needs and sustainability goals.

Teletrac Navman is committed to empowering fleet operators with the necessary tools, technology, and intelligence to confidently manage this transition, as Barney Goffer, Product Manager of Fleet Energy Solutions at Teletrac Navman aptly affirms:

“Teletrac Navman remains at the forefront of this transformation, equipping fleet operators with the tools, technology and intelligence they need to navigate this transition confidently. As such, we will continue to provide real-time visibility, performance analytics and sustainability-focused solutions in our commitment to helping businesses drive meaningful change and build a more sustainable future.”

For further reading on the subject, take a look at our Why Businesses Are Moving to Electric & Low-emissions Vehicles article.